What Is Tesla Actually Worth ?

Breaking down Tesla's cash flow, AI investments, Robotaxi optionality and intrinsic value.

Inside This Report

How Tesla continues generating billions in operating cash flow despite weaker vehicle margins

Why Tesla’s free cash flow story looks very different from its headline cash balance

The hidden impact of AI infrastructure, Robotaxi, batteries and factory investments

Tesla’s growing liquidity position and what management is doing with that capital

Why Energy may become Tesla’s second major profit engine

The importance of FSD subscriptions, autonomy and Robotaxi optionality

Whether Tesla’s current valuation can be justified by traditional cash flow metrics

Full DCF valuation with bear, base and bull scenarios

Why Buy Tesla Now: the strongest arguments for the bull case

Why Not Buy Tesla Now: the biggest risks investors may be ignoring

What the market is actually pricing in at a $1.5 trillion valuation

What Tesla’s next decade could realistically look like

Free Preview

Few companies generate more debate than Tesla.

For some investors, Tesla is still primarily an EV manufacturer.

For others, it is becoming an AI company, a robotics company, an energy company, or eventually a Robotaxi platform.

The reality is that today’s valuation reflects all of those possibilities simultaneously.

That is what makes Tesla both fascinating and incredibly difficult to value.

The company clearly generates cash.

The question is whether the future cash flows implied by the current valuation are realistic.

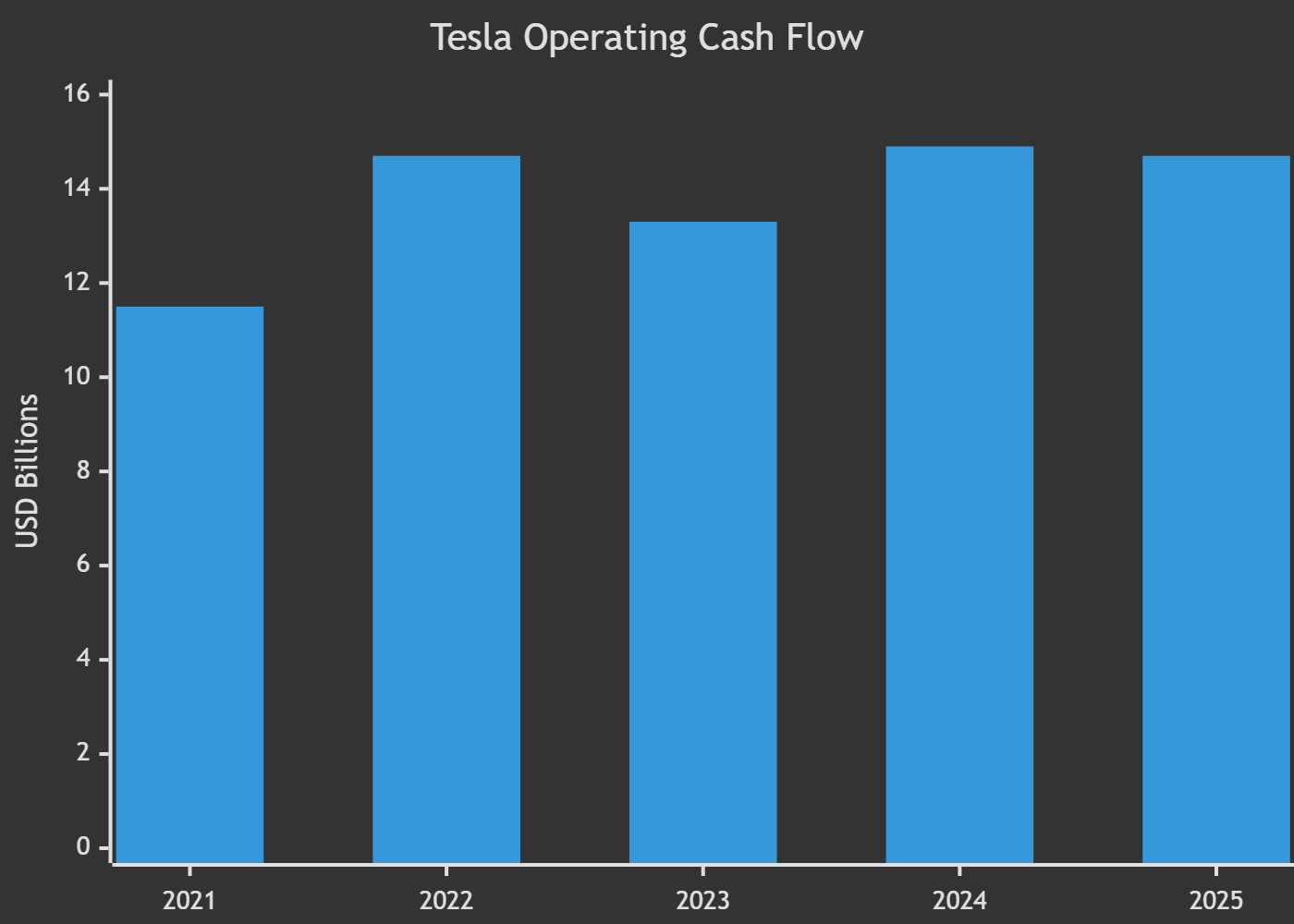

Tesla’s Cash Generation Remains Strong

Despite years of price cuts, margin pressure and growing competition, Tesla continues generating substantial operating cash flow.

The business remains cash-generative at its core.

Over the last five years Tesla produced roughly $68 billion of cumulative operating cash flow.

That is not the profile of a company struggling financially.

However, operating cash flow only tells part of the story.

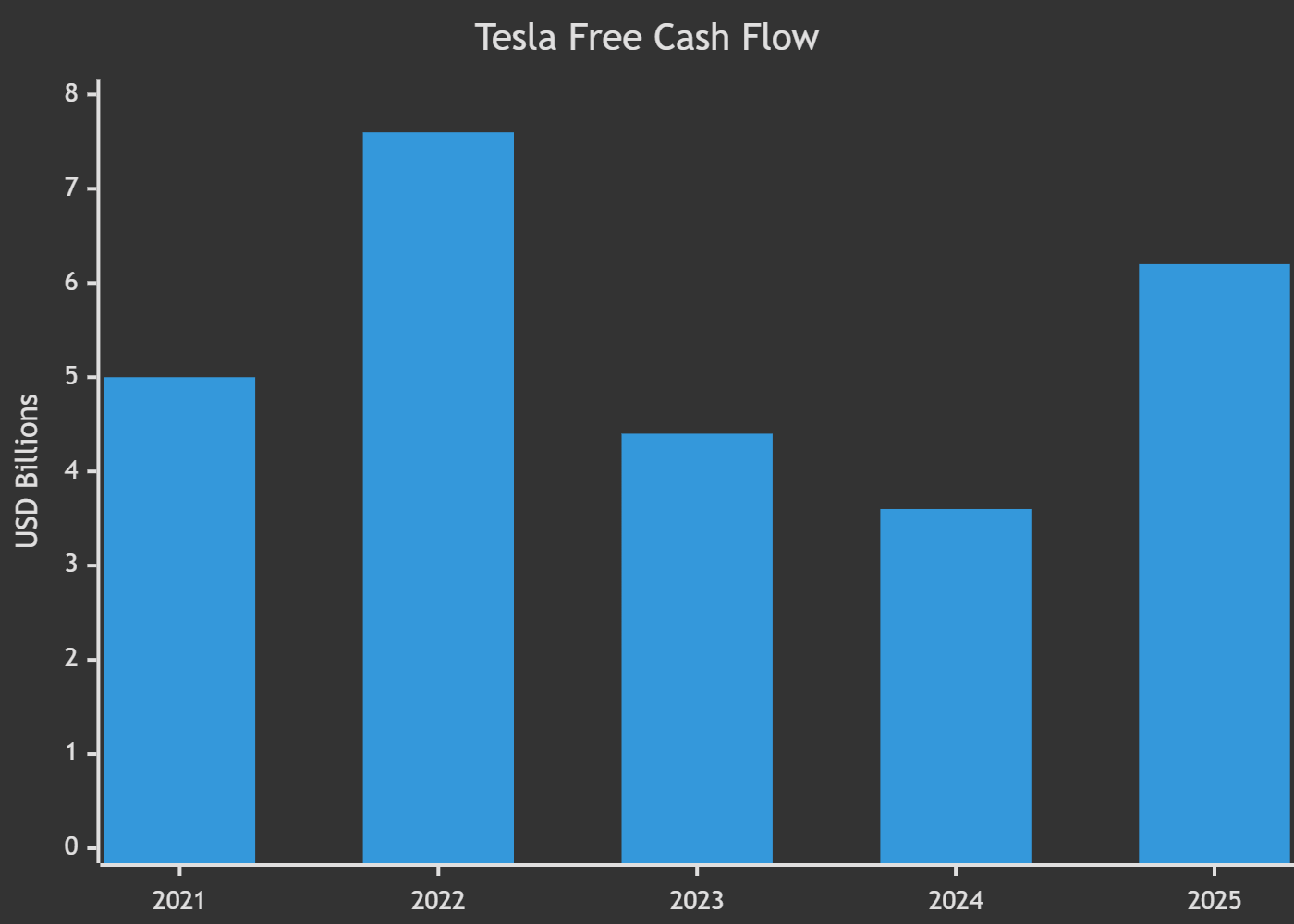

Why Free Cash Flow Matters More

The market often focuses on Tesla’s cash balance.

But investors ultimately get paid from free cash flow, not operating cash flow.

And this is where the story becomes much more complicated.

Tesla’s operating cash flow remained relatively stable.

Its free cash flow did not.

The reason is simple:

Tesla is entering another major investment cycle.

Cash Accumulation Has Become Cash Deployment

For years Tesla focused on strengthening the balance sheet.

Today the company appears focused on deploying that capital.

Management is simultaneously investing in:

AI infrastructure

Robotaxi deployment

FSD development

Energy storage

Battery manufacturing

Factory expansion

Robotics

The result is that future free cash flow may become significantly more volatile than investors became accustomed to during 2021-2022.

🔒 PRO SECTION — What You’ll Learn Below

PRO members can access:

✅ Tesla’s complete cash flow breakdown (2021–2026)

✅ The real quality of Tesla’s cash generation

✅ Why Tesla’s liquidity is stronger than most investors realize

✅ Why future free cash flow may become far more volatile

✅ The Energy business opportunity

✅ FSD, Robotaxi and autonomy economics

✅ Risks hidden inside Tesla’s financial statements

✅ Full DCF valuation model

✅ Bear, Base and Bull valuation scenarios

✅ Why Buy Tesla Now

✅ Why Not Buy Tesla Now

✅ What the market is actually pricing in today

Don’t miss the next cycle on TSLA 0.00%↑ and any of the other 85 tickers we constantly monitor, for just $7/month